H&M has closed nearly 1,000 stores since 2019. Zara has signed John Galliano. Unilever has spun off its entire foods division. Danone has just paid €1 billion for Huel. The industry is moving fast — and mostly sideways. Meanwhile, Uniqlo just keeps compounding. Nobody writes about it. That’s rather the point.

There’s a particular kind of business story that the industry loves. The dramatic pivot. The celebrity signing. The landmark deal that reshapes a portfolio and fills the trade press for weeks. These moves feel like strategy. They have narrative arc. They generate board-level excitement and investor day applause.

And then there’s the other kind of story. The one about a brand that didn’t pivot. Didn’t hire a couture legend. Didn’t merge, acquire or divest its way into a new identity. The one about a brand that just kept doing what it did — better, more consistently, more patiently — year after year, in almost complete silence.

That’s the Uniqlo story. And right now, in a week when a $45 billion merger just reshaped the global condiments shelf and a British meal replacement brand sold for €1 billion, it is exactly the story that brand leaders in CPG and beyond need to be sitting with.

Three fashion brands, three very different bets

To understand what Uniqlo has done, it helps first to look at what its closest peers have been doing instead.

H&M built its empire on volume, variety and speed. At its peak in 2019 it had over 5,000 stores globally. Since then it has closed nearly 1,000 of them — a painful, protracted rationalisation of a model that expanded faster than the economics could support. The closures are not failure in themselves; cutting a bloated estate is sensible management. But they are the visible symptom of a brand that grew by chasing scale rather than building something structurally sound beneath it.

Zara, under chair Marta Ortega Pérez, has made a different bet. Since 2022 it has been on a sustained push upmarket — premium campaigns, elevated store concepts, a series of designer collaborations. And then, announced just weeks ago: a two-year creative partnership with John Galliano, the couturier who defined Dior in the 1990s and rebuilt his reputation at Maison Margiela. The first collection arrives in September 2026. It is bold, conspicuous, and expensive — and it arrives at a moment when Zara’s underlying revenue growth slowed to just 1% in fiscal 2025, its weakest in a decade outside of the Covid year.

H&M – Nearly 1,000 stores closed since 2019. Restructuring a footprint built for a volume model the market no longer supports. New CEO, new direction.

Can discipline hold as volumes soften?

Zara – Signed John Galliano for a two-year creative partnership. Betting on borrowed prestige to build pricing power as revenue growth stalls at 1% in FY2025.

What happens when the headlines fade?

Uniqlo – No pivot. No celebrity deal. No repositioning. Product, discipline and compounding growth: revenue up 14.8%, business profit up 31% in Q1 2026.

Nothing to unwind

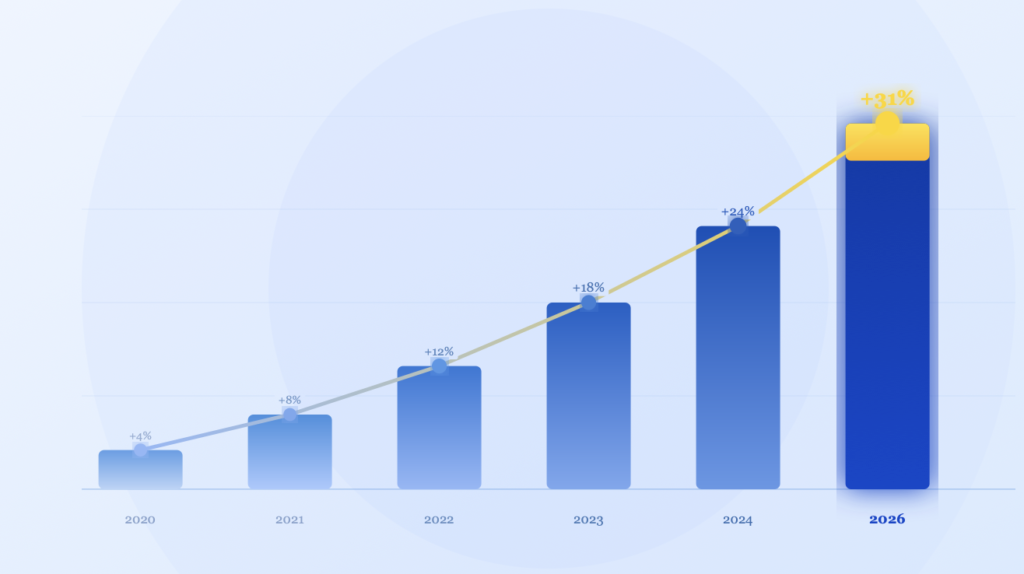

And Uniqlo? Fast Retailing reported record results in Q1 2026: revenue up 14.8% to over one trillion yen, business profit up 31%. Its international division — the engine of future growth — saw revenue rise 20.3% and profit surge 38%. Driven, in the company’s own words, by “the successful development and marketing of products that captured customer demand.” Not a designer. Not a repositioning. Products that captured customer demand. That’s it.

The boring strategy that keeps winning

Uniqlo’s model is, by the standards of fashion, almost aggressively dull. It doesn’t chase trends. It doesn’t rotate its range every few weeks. It doesn’t produce runway collections or court celebrity endorsers. What it does instead is engineer: functional fabrics that solve real problems for real people, refined incrementally over years until they work almost perfectly.

HeatTech. AIRism. LifeWear. These aren’t marketing slogans layered over commodity products. They are the result of sustained R&D investment and manufacturing discipline, executed at a scale that gives Uniqlo a cost and quality advantage most competitors simply cannot replicate. When Uniqlo launches a new iteration of HeatTech, it isn’t chasing a trend. It’s improving something that already works. That is a fundamentally different activity — and it builds a fundamentally different kind of brand equity.

Capped range – Around 1,000 core SKUs. Every product earns its place. No spray-and-pray variety. The discipline produces better inventory control, fewer markdowns and higher full-price sell-through.

+31% business profit growth, Q1 2026 — driven by product, not repositioning

Material obsession – HeatTech. AIRism. LifeWear. Proprietary fabrics engineered to solve problems. R&D spend goes into what you wear — not into cultural permission slips or borrowed prestige.

+38% profit growth, Uniqlo International, Q1 2026

Designer integration – Designers serve the product system, not the other way around. The goal, as creative director Clare Waight Keller has described it: finding the perfect version of a garment, not producing 20 and hoping 10 sell.

17% operating profit margin, H1 2025 — exceptional for global apparel at scale

source – Fast Retailing H1 2025 results

These results were achieved, as the company explicitly notes, through fewer discounts and better gross margin — not promotional mechanics. This is the compounding effect of disciplined brand strategy. When you don’t train customers to wait for deals, you sell more at full price. When you sell more at full price, margin expands. When margin expands, you invest more in product. And when the product keeps improving, customers return — not because of a flash sale, but because the thing works.

“The product is the story — not a borrowed name. That distinction is simple to state and extraordinarily difficult to sustain.”

Now look at what’s happening in CPG

The Uniqlo story would be instructive in any period. But it becomes urgent when set against what has happened in the CPG world in just the last few weeks — a compressed, almost dizzying series of moves that reveal an industry under enormous strategic pressure.

Unilever Foods + McCormick – Announced 31 March 2026 · ~$45 billion deal

Unilever spins off its entire foods division — Hellmann’s, Knorr, Marmite — to focus on beauty, personal care and wellness. McCormick gains scale in condiments and global foodservice. The rationale: costs, distribution reach and portfolio focus.

What happens to Hellmann’s brand identity inside a spice giant?

Danone acquires Huel – Announced 23 March 2026 · €1 billion

Danone buys one of Britain’s most values-driven, community-led nutrition brands — built over ten years on DTC loyalty and a passionate following — for €1 billion. The stated logic: scale, R&D, distribution. Huel retains its CEO and operates autonomously.

Does Huel’s community follow the brand into corporate ownership?

These are not marginal moves. They are tectonic shifts in how the largest CPG companies in the world are thinking about their portfolios — driven by cost pressure, the need for data, distribution scale, and the desire to access the growth that smaller, more agile, more values-led brands have been generating while the incumbents stood still.

The strategic logic is clear and defensible in every case. What is less clear — and what the Uniqlo story forces us to ask — is what gets lost in the transaction.

The question nobody is asking loudly enough

Huel is a genuinely interesting brand. It was built over ten years on a simple but powerful idea: nutritionally complete food, made sustainably, sold direct to people who actually cared about what they were putting in their bodies. Its community didn’t form around a discount. It formed around a mission. The brand had, and still has, the kind of authentic values-alignment that large CPG companies spend fortunes trying to manufacture and almost never achieve.

Danone’s CEO has said that Huel is “smack on where the consumer is going.” He is right. But the question is not whether Danone can see Huel’s value. It is whether a company of Danone’s scale and structure can preserve it. The soul of a founder-led, DTC brand is not a balance sheet item. It doesn’t appear in the acquisition multiple. And it is, historically, one of the first things to erode once the reporting lines change and the procurement team starts asking questions about ingredient sourcing margins.

The same question hangs over the McCormick/Unilever Foods deal. Hellmann’s and Knorr are not just condiments. They are brands with genuine household recognition, decades of consumer trust and — in many markets — strong emotional connections. How those brands are managed, invested in and spoken to inside a combined entity targeting $600 million in cost savings will determine whether that trust compounds or quietly erodes over the next five years.

This is the pattern that the Uniqlo story illuminates from a different angle. Unilever, in acquiring Dr. Squatch, Wild and K18, is doing precisely what large brands do when they want access to the authenticity and growth that smaller brands generate. The risk is the same in every case: the asset being acquired is partly cultural, not just commercial. The customer base that made the brand worth buying was loyal to something specific — a founder’s voice, a set of values, a way of talking to them that felt human. That doesn’t automatically survive integration.

The brands that avoid this problem are the ones that never needed to solve it — because they built something so structurally sound, so product-led and so consistently executed that they became the acquirer of choice rather than the acquisition target.

The risk of borrowed equity — in fashion and in food

There is a through-line connecting Zara’s Galliano bet and the wave of CPG consolidation: both are, at their core, attempts to acquire something that cannot easily be built from scratch. Zara is acquiring cultural authority. Danone is acquiring community loyalty and values-alignment. McCormick is acquiring distribution scale and brand recognition. All of it is rational. All of it carries the same underlying risk.

Borrowed equity has a shelf life. The Galliano headlines will drive coverage through 2026 and into 2027. The question is what remains of Zara’s pricing power when the collaboration concludes and the stores still feel, to most of its customers, exactly the same as they did before. Similarly, Huel’s community will give Danone a honeymoon period. The test comes when the first cost optimisation decision affects an ingredient that Huel’s customers care about — and they will care, because that’s precisely why they chose Huel over every cheaper alternative.

“The brands that win long-term aren’t the ones making the loudest moves. They’re the ones that never needed to make them.”

What this means for brand leaders right now

The Uniqlo model is not a call to be passive or to resist change. Fast Retailing is relentlessly active — in product innovation, in geographic expansion, in the careful integration of designers into a product-led system. What it resists is the particular kind of activity that substitutes noise for progress: the repositioning that doesn’t change the underlying product, the acquisition that buys growth without building it, the celebrity partnership that generates headlines without changing customer behaviour.

For CPG brand leaders watching this week’s deals unfold, the most useful question is not “should we be acquiring?” or “should we be divesting?” It’s the harder one: do we have the product story, the customer relationships and the internal capability to compound without needing to? Because the brands that are being bought right now are being bought precisely because someone else decided they didn’t.

Uniqlo doesn’t need to acquire a values-led brand. It is one. It doesn’t need to buy a DTC community. It built one. It doesn’t need a designer’s name to signal quality. The product does that. That structural advantage — built quietly, patiently, over decades of disciplined execution — is not luck. It is the result of a clarity of purpose and a standard of capability that most organisations find genuinely difficult to sustain under commercial pressure.

The capability question

Which is, ultimately, where the Uniqlo story becomes most useful for leaders in CPG. The discipline it describes — capping your range, investing in product over promotion, building genuine customer relationships rather than buying them — is not technically complex. It is organisationally hard. It requires commercial teams that think differently, marketing functions that know how to tell a product story rather than run a promotional calendar, and leadership that is willing to accept short-term noise in pursuit of long-term compounding.

That capability doesn’t come from a strategy deck. It has to be built — deliberately, with investment in the right thinking and the right people. The brands that will look back on this period clearly are the ones that used the disruption around them not to make the next big move, but to quietly build something that doesn’t need to be unwound.

Nothing to reposition. Nothing to integrate. Nothing to defend.

Just a product that works, priced fairly, executed consistently — and a team with the capability to keep making it better.

That’s the Uniqlo lesson. It was never really about fashion.

Cognitive Union works with large B2C and B2B businesses to build the commercial skills, digital fluency and customer-first thinking their teams need to perform — closing the capability gaps that sit between where teams are today and where the business needs them to be.

Lead. Don’t follow.

Find this blog useful? Sign up to our email newsletter (bottom of this page) where you can receive articles like this and other insights (not publicly published), and you can also follow us on LinkedIn.